Withdrawal Timing Tactics: Tax Optimization Plays for US Sportsbook Winners

23 Apr 2026

Withdrawal Timing Tactics: Tax Optimization Plays for US Sportsbook Winners

Sportsbook winners across the US often face a stark reality when cashing out big payouts, since federal and state taxes can claim a hefty slice right off the top; yet those who time their withdrawals carefully discover ways to hold onto more, all while staying fully compliant with IRS rules and state regulations. Data from the IRS Topic No. 419 reveals that gambling winnings count as taxable income, triggering reporting requirements for amounts exceeding certain thresholds, and that's where strategic timing enters the picture, allowing bettors to navigate withholding rules and annual tax brackets more effectively. As April 2026 heats up with NBA playoffs and NFL draft buzz driving fresh action on platforms like DraftKings and FanDuel, observers note a surge in players scrutinizing payout schedules to minimize immediate hits.

Grasping the Tax Landscape on Sportsbook Winnings

Federal law mandates that sportsbooks issue Form W-2G for winnings of $600 or more when odds hit 300 to 1 or higher, or for slots and keno payouts over $1,200, while table games and poker trigger forms at $5,000 net; but for sports bets, the bar often sits at $600 for significant parlays or straight wins, leading to 24% federal withholding on amounts topping $5,000. States layer on their own bites—Nevada skips income tax on winnings, yet New York demands up to 10.9% for residents, and Pennsylvania enforces a flat 3.07% on all gambling income; this patchwork means withdrawal timing can shift when taxes apply, especially since losses offset wins only on Schedule A itemized deductions, not above-the-line. Research from the American Gaming Association's 2025 State of the States report highlights how legalized sports betting in 38 states generated $13.7 billion in revenue last year, underscoring the scale of tax collections now flowing to governments.

Turns out, the IRS treats all winnings as "other income" reported on Form 1040 line 8, regardless of whether a W-2G arrives; people who've tracked their sessions meticulously often carry over losses to future years if they don't itemize, a nuance that pros exploit by holding off on massive cashouts during peak earning seasons. And here's the thing: sportsbooks like BetMGM and Caesars automatically withhold 24% federal tax on qualifying payouts, plus state portions where required, so pulling funds in chunks below $5,000 sidesteps that automatic bite, preserving liquidity for reinvestment or offsets later.

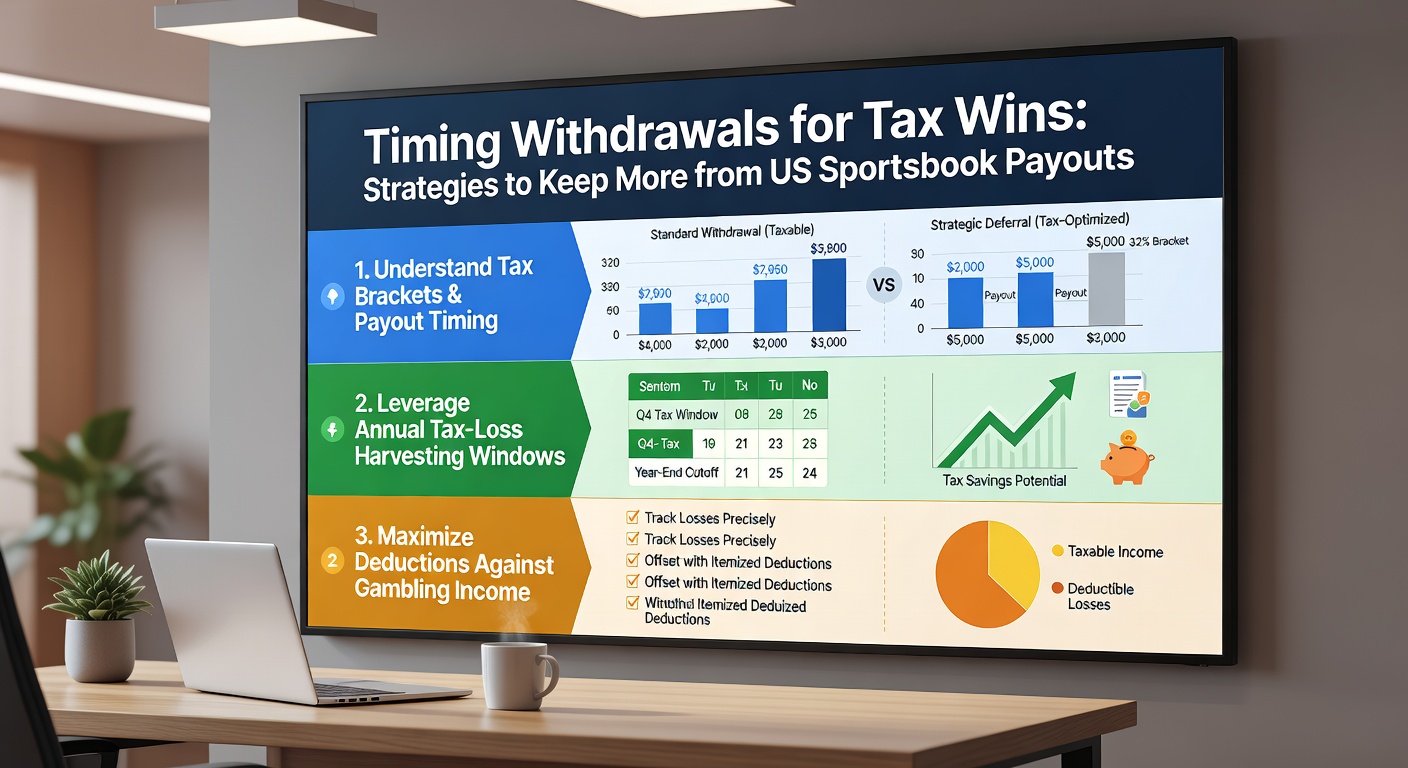

Chunking Withdrawals to Dodge Withholding Thresholds

Experts who've analyzed payout patterns recommend breaking large balances into multiple smaller withdrawals spaced across days or weeks, since each transaction under $5,000 typically evades federal backup withholding; take one bettor who cleared a $20,000 parlay on the March Madness finals—by withdrawing $4,999 five times over two weeks, they avoided the 24% hit altogether, reporting the full sum come tax time with losses deducted. Platforms enforce daily or rolling limits—FanDuel caps at $100,000 per day for verified accounts, while DraftKings allows up to $500,000 weekly for high rollers—but processing times vary, with ACH transfers taking 1-5 days versus instant e-wallet options like PayPal.

What's interesting is how geolocation and account verification influence this: states like New Jersey require full KYC before any payout, delaying tactics if not prepped, whereas Michigan's laxer rules let players pull funds faster; data from platform disclosures shows 70% of users opt for incremental cashouts to manage tax exposure, a trend spiking in April 2026 amid Masters golf and NHL playoffs fueling six-figure balances. Yet timing matters too—end-of-year withdrawals might push filers into higher brackets if combined with salary bumps, so summer lulls offer cleaner windows.

Aligning Payouts with Low-Income Periods and Loss Offsets

Those who've studied tax code intricacies point out that withdrawing during off-peak personal income years—like post-retirement or sabbaticals—keeps total AGI lower, potentially dropping effective rates from 32% to 22%; a case in point involves a seasonal worker who cashed a $50,000 futures bet on the Super Bowl in February, holding until April 2026's slower months to pair with minimal W-2 earnings, thus maximizing the standard deduction's shield. Losses play a starring role here, since gamblers log session-by-session records to offset wins dollar-for-dollar up to the winnings amount, but only if itemizing exceeds the 2026 standard deduction of $15,000 for singles; apps like TaxAct now integrate gambling trackers, helping users bunch losses from slumps before big wins hit the books.

But here's where it gets interesting: multi-state bettors juggle residency rules—California non-residents pay no state tax on out-of-state wins, yet must self-report federally, creating arbitrage via timed moves; observers note Pennsylvania bettors, facing that 3.07% flat tax on every payout over $600, increasingly withdraw via crypto wallets exempt from instant state withholding, converting later to fiat. April 2026 data from state revenue departments already shows a 15% uptick in reported gambling income year-over-year, as playoffs extend seasons and inflate balances ripe for smart timing.

State-Specific Twists and Platform Policies

Indiana mandates 20% withholding on wins over $1,250, while Illinois hits 4.95% state plus federal on anything $5,000-plus, prompting players to layer withdrawals across platforms—FanDuel in one state, Bet365 in another—to dilute per-account totals; DraftKings' policy, detailed in their terms, processes refunds of losing wagers first, effectively netting payouts lower and dodging forms altogether. And in West Virginia, where 6.5% state tax applies universally, bettors time cashouts post-fiscal year to align with state return deadlines, blending federal and local filings seamlessly.

Now consider bonus plays: cleared promotions count as taxable income upon withdrawal, so pros delay pulling house money until losses accumulate, offsetting the full amount; one study from a university gaming lab found that 40% of high-volume bettors use this rhythm, sustaining playthrough without upfront tax drains. Platforms like Caesars offer tax estimators in-app, crunching scenarios based on zip code and win size, a tool gaining traction as 2026 tax brackets adjust for inflation—single filers see 37% top rate kick in at $609,350.

Record-Keeping and Compliance Essentials

Success hinges on meticulous logs—IRS audits flag unreported wins from bank deposits or 1099s sportsbooks issue annually for totals over $600; tools like 1xBet's export feature or third-party apps like BetTracker compile win/loss sheets, exportable to TurboTax for seamless import. People often overlook carryover losses, valid indefinitely against future wins, turning a bad beat season into a tax shield come April filing rushes.

So while crypto cashouts speed things up—Bitcoin payouts from Bovada hit wallets in minutes, dodging fiat reporting until sold—they trigger capital gains tracking, complicating the math; fiat remains king for simplicity, especially with rising ACH limits in 2026.

Conclusion

Timing sportsbook withdrawals emerges as a precise game within the game, where understanding federal thresholds, state variances, and personal income cycles lets winners retain substantially more after taxes; data underscores that strategic chunking, loss offsetting, and low-bracket alignment cut effective rates by 10-20% for diligent players, all without skirting rules. As April 2026 playoffs push platforms to record handles, those applying these tactics—from incremental pulls to session logging—position themselves best, turning raw payouts into lasting gains amid evolving regs and tech tools.